Tax Foundation Response to UN Request for Public Input on Inclusive and Effective Tax Cooperation

Sound tax policy should be based on the principles of simplicity, stability, transparency, and neutrality.

4 min read

Daniel Bunn is President and CEO of the Tax Foundation. Daniel has been with the organization since 2018 and, prior to becoming President, successfully built its Center for Global Tax Policy, expanding the Tax Foundation’s reach and impact around the world.

Prior to joining the Tax Foundation, Daniel worked in the United States Senate at the Joint Economic Committee as part of Senator Mike Lee’s (R-UT) Social Capital Project and on the policy staff for both Senator Lee and Senator Tim Scott (R-SC). In his time in the Senate, Daniel developed legislative initiatives on tax, trade, regulatory, and budget policy.

He has a master’s degree in Economic Policy from Central European University in Budapest, Hungary, and a bachelor’s degree in Business Administration from North Greenville University in South Carolina.

Daniel lives in Halethorpe, Maryland, with his wife and their three children.

Sound tax policy should be based on the principles of simplicity, stability, transparency, and neutrality.

4 min read

Different taxes have different economic effects, so policymakers should always consider how tax revenue is raised and not just how much is raised.

4 min read

Designing tax policy in a way that sustainably finances government activities while minimizing distortions is important for supporting a productive economy.

5 min read

The process leading to the global minimum tax has been messy, and the mess will likely continue for years to come. New revenues are hardly a salve for the setback they represent.

7 min read

As it stands, Pillar One would usher in the end of many digital services taxes (though perhaps not all) at the cost of increased complexity (in an already complex and uncertain system).

4 min read

the Inflation Reduction Act gives us a glimpse into a future where the U.S. and EU opt for protectionist tax and trade policies rather than implementing principled tax policies and reducing trade barriers between allies.

5 min read

While there are many factors that affect a country’s economic performance, taxes play an important role. A well-structured tax code is easy for taxpayers to comply with and can promote economic development while raising sufficient revenue for a government’s priorities.

41 min read

For many years, the UK has adopted a strikingly ungenerous approach to capital cost recovery – the ability of firms to write off investment against tax. This has coincided with consistently low levels of business investment. The super-deduction, which has temporarily made the UK tax system much more supportive of capital investment in plant and machinery is set to expire.

34 min read

Carryover tax provisions help businesses “smooth” their risk and income, making the tax code more neutral across investments and over time.

3 min read

In an already-challenging economic environment, new UK Prime Minister Liz Truss must get tax rates correct to avoid over-burdening a population and business sector facing immense uncertainty. Focusing only on rates while ignoring the base misses an opportunity for real, pro-growth reform.

4 min read

With continued concerns over inflation, individuals may be wondering how their tax bills will be impacted. Less than half of OECD countries in Europe automatically adjust income tax brackets for inflation every year.

2 min read

The phaseout of 100 percent bonus depreciation, scheduled to take place after the end of 2022, will increase the after-tax cost of investment in the U.S. Permanently extending it would increase long-run economic output by 0.4 percent and increase employment by 73,000 FTE jobs.

20 min read

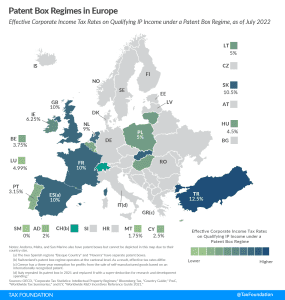

Patent box regimes (also referred to as intellectual property, or IP, regimes) provide lower effective tax rates on income derived from IP. Most commonly, eligible types of IP are patents and software copyrights. Currently, 13 of the 27 EU member states have a patent box regime.

3 min read

Pillar One Amount A is meant to reallocate taxable profits of large multinationals, mitigate double taxation of profits, and avoid a harmful tax and trade war.

5 min read

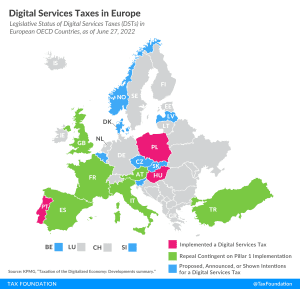

About half of all European OECD countries have either announced, proposed, or implemented a digital services tax.

7 min read

Over the course of the last year, it has become clear that Democratic lawmakers want to change U.S. tax rules for large companies. However, as proposals have been debated in recent months, there are have been clear divides between U.S. proposals and the global minimum tax rules.

6 min read

While the global minimum tax gets much attention in the media, there is another significant piece to the deal.

6 min read

Congress should prioritize evaluation of recent international tax trends and the model rules and adjust U.S. rules in a way that supports investment and innovation and moves towards simplicity.

27 min read

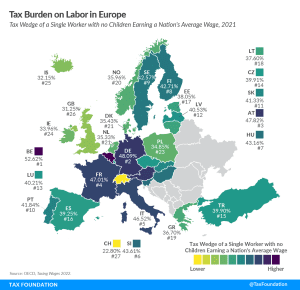

To make the taxation of labor more efficient, policymakers should understand the inputs into the tax wedge, and taxpayers should understand how their tax burden funds government services.

3 min read

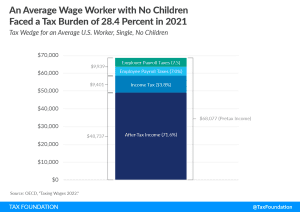

Although the U.S. has a progressive tax system and a relatively low tax burden compared to the OECD average, average-wage workers still pay nearly 30 percent of their wages in taxes.

4 min read